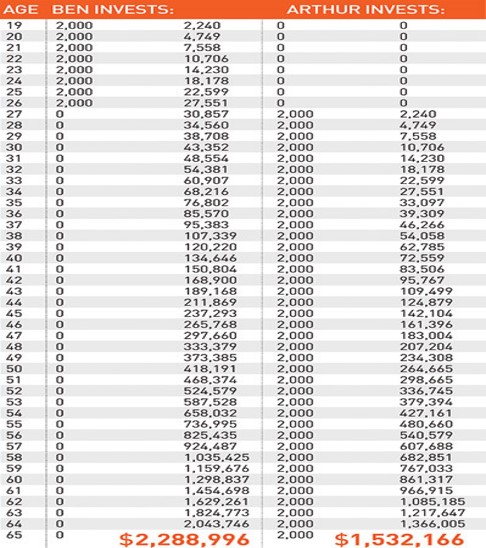

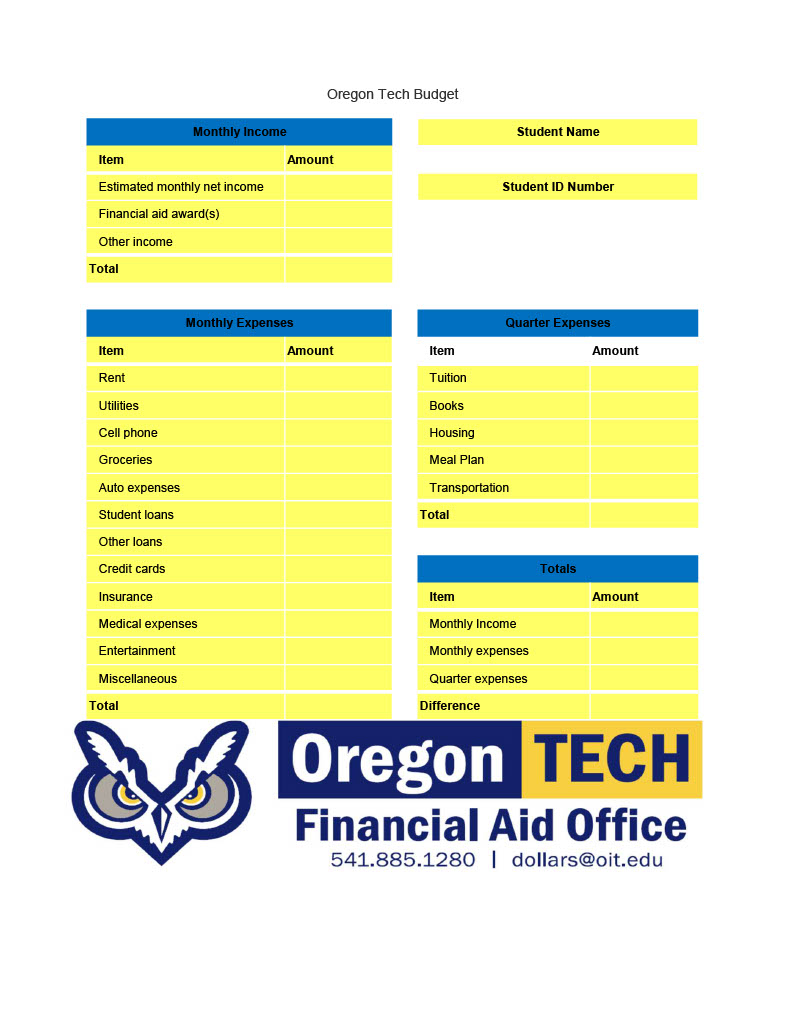

A Hands-On Approach to Funding Your Future Financial Literacy ProgramPlease see below for the Zoom link, dates, and times. All events will be available through Zoom Apr. 9th 3pm Accepting Job Offers -Library, Lower Mezzanine “the Den”Apr. 15th 3pm Understanding Mortgages -Library, Lower Mezzanine “the Den”Apr. 22nd 3pm Key Bank Financial Literacy -Library, Lower Mezzanine “the Den” -Portland Metro Room 106May 12th 3pm Game of Kahoot -Library, Lower Mezzanine “the Den” Investing Image Compound Interest Calculator Presentations Watch the following short videos to get an idea of how financial aid can work for you. They cover a broad range of topics including required documents, FAFSA, grants, scholarships, timeline, and more! Documents Budget Activities Chart Credit Reporting Bureaus Experian Equifax TransUnion Opt-Out Option: National Do Not Call Registry - Register cell phones and landlines to stop telemarketing phone calls